Gaming

Are Fortnite-style branded collaborations the key to Overwatch 2’s future success?

It’s been a rough month for the launch of Overwatch 2. In the first few days of its release, Blizzard’s long-awaited sequel to the 2016 team-based shooter was plagued with connection issues, leaving millions of players unable to enter matches. While many of the problems relating to server issues have now been addressed, Blizzard now has another challenge on its hands: making enough sales from microtransactions to support the franchise’s move to a free-to-play model.

So far, that’s been pretty difficult. Overwatch 2’s recent Halloween event, Halloween Terror, introduced a variety of themed character and weapon skins into the game for the ‘discounted’ price of 2000 Overwatch Coins each, roughly the equivalent of $20. A legendary skin for the character Kiriko was available for 2600 Overwatch Coins, a discount on the original price of 3700 Overwatch Coins. As you might imagine, this is already causing upset amongst some players, especially as this year’s Halloween update removed the option to earn unlockable skins simply by progressing through the game.

Evidently, some players aren’t willing to spend over $20 for an alternative outfit for their character. However, we do know that players are more than happy to spend roughly the same price in other free-to-play games such as Fortnite to unlock characters from popular franchises, whether that’s Goku from Dragon Ball Z or Marvel’s Spider-Man. This is something that Jon Spector, Overwatch’s commercial leader and vice president at Blizzard, seems well aware of, according to a recent interview with GameInformer.

In the interview, Spector announced that while he isn’t a Fortnite player, he thinks it’s ‘super cool’ and ‘awesome’ to see branded collaborations such as Naruto appear in Fortnite.

“As we look at the Overwatch 2 space, those are things that we’re interested in exploring,” he says.

So, with Overwatch 2’s current monetisation strategies leaving a lot to be desired, could we see a shift towards branded collaborations as a core monetisation strategy rather than the traditional legendary and epic skins? Dropping the price of skins and embracing Fortnite-style collaborations would make a lot of commercial sense for Overwatch 2, especially as the company still seems torn on its pricing, according to a recent survey sent out to select players.

We know that Fortnite’s collaborations with the likes of Marvel, NFL, Nike and Ferrari have been hugely successful for Epic, largely due to the amount of revenue they generate from the sale of cosmetic items such as skins, emotes, banners and emoticons. As an example, the game’s collaboration with NFL resulted in 3.3 million NFL-themed skins being sold for $15 each in November and December 2018, according to leaked court documents from the Apple v Epic case. That’s nearly $50 million in revenue.

The big question now is how easily Overwatch 2 can replicate Fornite’s primary business model, and how well-suited these collaborations are for the Overwatch brand.

One of the biggest challenges facing Overwatch 2 is the fact it’s a hero-based shooter, with each hero boasting their own unique set of skills, traits and playstyles. As is often the case with team-based shooters, players often find themselves favouring specific heroes, whether that’s offensive heroes or defensive heroes that suit their preferred styles of playing.

This means Overwatch 2 will have to think carefully about how it rolls out branded collaborations. As an example, will a Marvel collaboration introduce special themed skins for every single hero in the game, or will it introduce a new limited-time character into the game? The introduction of any new character will have to be calculated carefully, so it doesn’t negatively impact the balance of existing characters.

It’s more likely that Overwatch 2 will introduce themed skins rather than new characters such as those seen in Dragon Ball Z. Depending on the popularity of the IP that Overwatch 2 pursues, I suspect players will be more susceptible to investing $15 or $20 into a skin that turns their favourite Overwatch hero into an alternative version of their favourite anime, film, TV or comic book characters, whether that’s Spider-Man, Darth Vader or one of The Transformers.

The hero-based mechanics of Overwatch 2 could also mean skins are only available for specific characters. While this might cause backlash amongst some fans at first, it could also open up alternative revenue streams. As an example, the style and appearance of the tank hero Reinhardt lends itself well to a Transformers skin. Players that don’t typically choose Reinhardt but are huge Transformers fans may be tempted to purchase a Transformers skin for him and start using him more. In turn, this could lead to a knock-on effect for players who go on to purchase Reinhardt’s wider cosmetic items.

There’s no denying that Overwatch 2 is a great game; the reviews have been overwhelmingly positive. If Overwatch 2 continues to struggle with monetisation models, branded collaborations like those in Fortnite might be the answer to its future success. But taking an established franchise that previously carried a full-price retail tag and moving it over to a free-to-play model is no easy task.

Key considerations when choosing your target IP

If you’re a game developer looking to emulate Fornite’s IP success, there are a few things you need to consider before bringing IP into your game.

- Don’t pick a target IP just because it’s a really popular brand or character. Look at your game and your players and ask yourself if it’s something that will resonate with them. For example, a clever partnership between The Walking Dead and State of Survival brought 20 million new players to the game. So a good understanding of your player demographics is a must. Be prepared to prove this to the license holders, too, as they’ll be just as interested to know if there’s any audience overlap.

- It may sound simple, but make sure you do your homework. Different IP rights holders can have very different priorities and strict requirements for usage. Bigger properties, especially ones that are popular with children, can be especially stringent as its in the holders interests to carefully limit their use. So, it’s up to developers to demonstrate their ability to comply with them. Being prepared can give you a huge advantage, and help clear some of the initial screening phases and get in front of the right decision-makers.

- There are more ways to integrate IP into your game than ever. So think carefully about your main goals, as simpler in-game items, like cosmetics and skins, are often much easier to negotiate with rights holders due to less complicated terms, plus, lighter development and creative costs can make them much quicker to roll out. FIFA 23 recently brought Apple TV’s Ted Lasso as well as Marvel cards to Ultimate Team, with these simple, smart deals opening the door for more collaborations in future.

Written by: Rachit Moti, founder and CEO at Layer Licensing, a licensing marketplace that helps game creators access brands, characters and stories that players love.

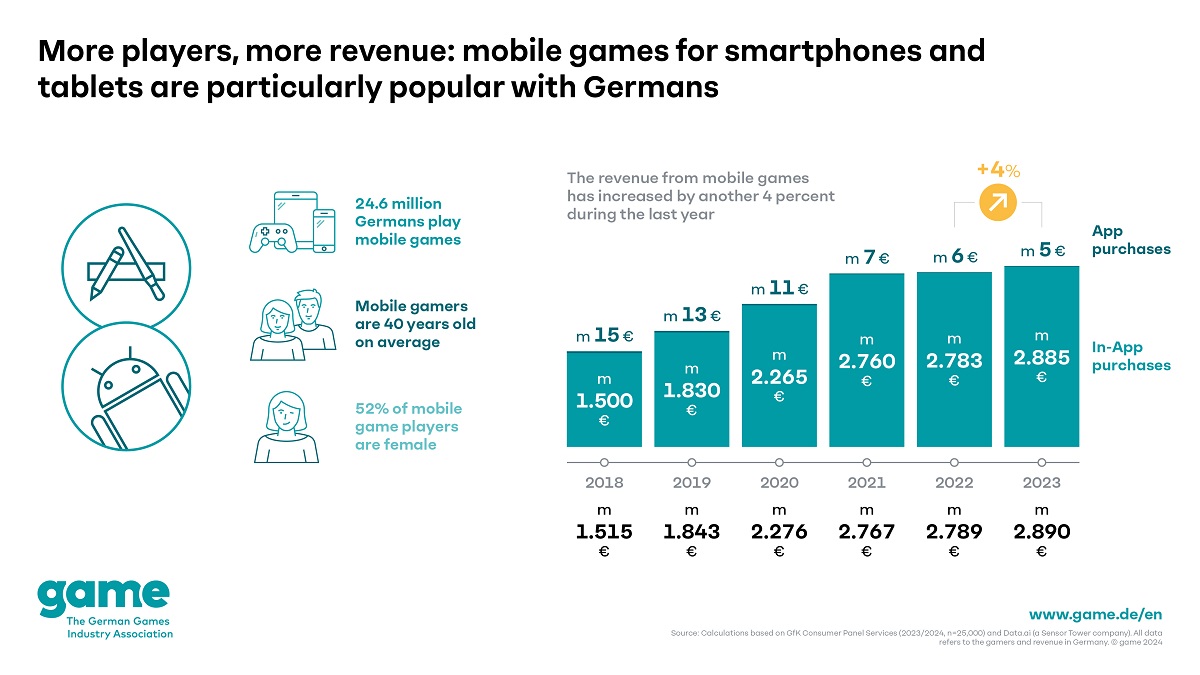

- Revenues from games apps grow in Germany by 4 per cent to over 2.9 billion euros

- Smartphones and tablets attract 300,000 additional players in twelve months

- ‘Mobile games often attract people with little or no experience of playing video games’

Games apps for smartphones and tablets continue to do well in Germany: revenues from mobile games grew by another 4 per cent to 2.9 billion euros within a year. This part of the games market has almost doubled since 2018, when revenues amounted to 1.49 billion euros. These are the figures released today by game – The German Games Industry Association, based on data collected by the market research company data.ai. Not only were games app revenues up, but the number of mobile game players also grew by 300,000 to 24.6 million in the space of a year. The average age of people who play video games on their smartphone in Germany is 40. Women tend to play more on smartphones and tablets (52%) compared to men (48%).

‘Games apps for smartphones and tablets are very popular among Germans,’ says Felix Falk, Managing Director of game. ‘Although we’ve been witnessing the unstoppable rise of the smartphone for almost a decade and a half, this is still an area of the game market that continues to grow. Mobile games often attract people with little or no experience of playing video games. The mobile gaming market has grown hugely over recent years: alongside classic casual games for spare moments, complex games and even esports titles are now also firmly established. This variety is unique and one of the strengths of games apps.’

A closer look at the mobile gaming market in Germany highlights the distinctive features of the sector: around 5 million euros – significantly below 1 per cent of total revenues – is generated by the sale of individual mobile games. Revenues from online gaming services on smartphones and tablets are significantly higher, amounting to 43 million euros or around 1 per cent. 98 per cent and therefore almost the entire revenue from games apps – 2.9 billion euros – is generated with in-app purchases. These include cosmetic enhancements for players’ own avatars along with virtual currencies and loot boxes or large story expansions.

Strong development of the German game market in 2023

The German games market showed significant overall growth again in 2023, with revenues from games, gaming hardware and online gaming services increasing by 6 per cent, to some 9.97 billion euros. This considerable rise follows a revenue increase of just 1 per cent in the preceding year. The largest drivers of this growth include game consoles and related accessories, as well as in-game and in-app purchases. At the same time, sales of gaming PCs and laptops saw clear declines in some areas.

Five teams have won over the Games Lift awarding committee with their game projects. On September 9, the Games Lift Incubator will start for them as a unique support program in Germany. Included is a one-year workshop and mentoring program with international industry experts and 15,000 euros in financial support, as well as room for collaboration and exchange with the other participating teams. More than 30 experts in game design, product development, pitching, business development, press relations and marketing from the Games Lift network will share their experience with the teams to give their projects a professional start. Starting this year, the program also offers participating teams a joint trip to an international industry event. The Games Lift Incubator is organized and implemented by Gamecity Hamburg on behalf of the Free and Hanseatic City of Hamburg.

A total of 21 teams and solo developers applied for the fourth Games Lift Incubator. The decision for the five participating teams was made by the awarding committee, consisting of Kristin von der Wense (Publishing Producer Daedalic Entertainment), Ole Schaper (Managing Director The Sandbox Hamburg (Sviper GmbH)), Heiko Gogolin (Managing Director Rocket Beans Entertainment) and Tobias Graff (Co-Founder, Programmer and CEO Mooneye Studios).

Margarete Schneider, Project Manager at Gamecity Hamburg, on the award committee’s decision: “We are delighted with the large number of applications for our incubator and the high standard of the pitch decks submitted once again. It is particularly pleasing that we are receiving more applications from outside Hamburg, who see the city as an attractive location for starting a new business. The Games Lift Incubator provides gaming start-ups with comprehensive starting support and enables them to forge connections in Hamburg’s diverse games scene.

The five winner projects and teams for Games Lift Incubator 2024:

- ForeFeathers by Team Honeybeak

- Frisia – Cozy Villages by Rouven Cabanis

- Light of Atlantis by Duck ‘n’ Run Games

- Pubcrawler by Triflgard

- Tiny Garden by Tales from the Garden

ForeFeathers by Team Honeybeak is a 3D Puzzle-Platformer where players slip into the role of a penguin, who explores the sky-high ruins of an ancient civilization of birds. Traversing the flying islands with the ancient powers of flight, solving tricky puzzles and keeping the penguin’s friends away from trouble are some main aspects of the game.

In Frisia – Cozy Villages by Rouven Cabanis the player gains control over an uninhabited Northsea island and is tasked with building a functional, yet cozy and beautiful little town. Inspired by the frisian architecture of the Dutch and German Northsea coast, Frisia aims to create a cozy gameplay experience in harmony with simple town-building and strategy game mechanics.

Light of Atlantis by Duck ‘n’ Run Games is a 2D puzzle metroidvania in which players take on the roles of various robots with individual abilities to explore the sunken ruins of Atlantis. By draining and releasing water into the various rooms, the robots shape their environment and improve their chances against different enemies. Light of Atlantis was part of the Gamecity Hamburg prototype funding in 2023 and received in the same year the German Computer Game Award (Deutscher Computerspielpreis) in the category “Best Prototype”.

Pubcrawler by Triflgard is a co-op PC game in which up to four players need to work as a team, to navigate a giant, mechanic, wandering pub through an apocalyptic wasteland. In the process, they must complete a variety of challenging tasks that can only be mastered as a team. Working together efficiently, pleasing the different guests and keeping a cool head even when the giant pubcrawler faces technical issues are the key to a successful journey.

In Tiny Garden by Tales from the Garden players slip into the role of a deity who fills a deserted planet with life. Together with their servants, a group of cute leaf creatures that must be protected from evil spirits, they plant a constantly growing garden. As soon as the garden is fully grown, the evil spirits can be soothed and the player can move on to the next planet in help.

MainStreaming, an iMDP INTELLIGENT MEDIA DELIVERY COMPANY, which is redefining the CDN market with its innovative Edge Network services, announced the appointment of Nicola Micali as its new Chief Customer Officer (CCO).

With a track record of improving processes and efficiency and creating go-to-market strategies, Harvard alumnus and former Akamaite, Nicola Micali joins MainStreaming with the goal of solidifying a customer-centric organisation that prioritises long-term relationships, customer experience (CX) and satisfaction, ensuring MainStreaming’s continued business growth and market leadership.

Nicola brings a wide range of professional experience as a Leader of Customer Success & Professional Services at Akamai for over 10 years, where he was responsible for services and overall revenue. He developed the services strategy for the Americas’ media & entertainment, gaming and partners verticals exceeding all revenue targets year after year. Nicola’s expertise in leading technical customer-facing teams has resulted in higher customer satisfaction and successful worldwide streaming events.

With a Master’s degree in Business Administration and Management from Harvard, Micali’s educational background further enhances his capability to lead and innovate in the Edge video technology sector. As Nicola steps in as CCO, he will play a pivotal role in guiding the entire customer lifecycle journey. His expertise in customer success positions him perfectly to lead MainStreaming’s efforts in providing world-class service to a global clientele.

MainStreaming’s CEO, Antonio G. Corrado, said: “QoS for our customers and QoE for end users are at the core of our streaming business. It is the best proxy for customer satisfaction for us. We are happy to welcome Nicola Micali, who demonstrates his expertise in customer success. Together, we are set to strengthen our commitment to being a customer satisfaction-oriented company, leveraging our world-class services directed to broadcast-quality standards that are requested by industry players.”

MainStreaming’s video delivery technology is meticulously developed in-house, offered as managed private Edge Network to help broadcasters, OTT TVs and content owners overcome the toughest challenges of live streaming at scale, addressing the limitations of classic CDN and enabling new application solutions on the Edge.

“I am honored to join a team that is on a mission to write a new chapter in video streaming delivery, setting new standards, and paving the way for the future of TV. I am ready to contribute to MainStreaming’s innovative approach and customer-centric philosophy. Together, we are set to revolutionize how the streaming industry approaches Edge Network architecture for live streaming, emphasizing a more distributed, ultra-low-latency, energy-efficient, and globally scalable design,” Nicola Micali said.

Win tickets to the BLAST Premier Fall Final: GG.BET is running a MEGA BLAST Competition for fans of СS2

MANCHESTER CITY TO MARK GLOBAL PARTNERSHIP WITH SUPER GROUP-OWNED BETWAY AT THE NEW YORK STOCK EXCHANGE

Acquiring a Curacao Online Gaming License in 2024: Comprehensive Analysis of Financial & Procedural Aspects with Costs & Timelines Detailed

IGT’s Gaming and Digital Business and Everi to Be Acquired Simultaneously by Apollo Funds in All-Cash Transaction

Interview with Bojoko’s Bingo Expert on the Affiliate Marketing Strategies and Bonuses That Covert

SOFTSWISS Shares Winning Sportsbook Strategies for the 2024 Olympic Games

Week 30/2024 slot games releases

iGATE showcases its White Label Solutions at iGB Live! Amsterdam

Fun88 Introduces T20 World Cup Special Offers

Download Minecraft version 1.22.0, 1.22.1 and 1.22.2 apk free

“Our Product is Young, Flexible, and Dynamic” – Anhelina Stasiuk on the Future of the SOFTSWISS Jackpot Aggregator

Gambling Commission’s new reporting requirements now in force

Live in Latvia! Spelet.lv and Hacksaw Gaming Celebrate New Launch Together

QTech Games wins Online Casino Provider of the Year Award for Africa

Revenant Esports crowned champions of OMEN VALORANT Challengers South Asia Split 2; to represent South Asia at VCT Ascension: Pacific

New Harm Minimisation Measures for Pubs and Clubs with Gaming Machines Come into Effect in New South Wales

-

Gambling in the USA5 days ago

Gambling in the USA5 days agoGaming Americas Weekly Roundup – July 15-21

-

Eastern Europe5 days ago

7777 gaming is now available on WINBET Romania

-

Gaming5 days ago

MainStreaming Announces Appointment of Nicola Micali as Chief Customer Officer

-

Industry News5 days ago

Safer Gambling Tools Use Hits Record High in 2023 – New Report from EGBA

-

Australia5 days ago

Australian eSports Star Joins Team Liquid

-

eSports5 days ago

INSPIRED LAUNCHES RE-PLAY ESPORTS™ FEATURING CS:GO IN PARTNERSHIP WITH KAIZEN GAMING

-

eSports5 days ago

NODWIN(R) Gaming ropes in Android as title partner for BGMS Season 3; to be powered by Garnier Men

-

Latest News5 days ago

Spinomenal shines again with Super Wild Fruits release